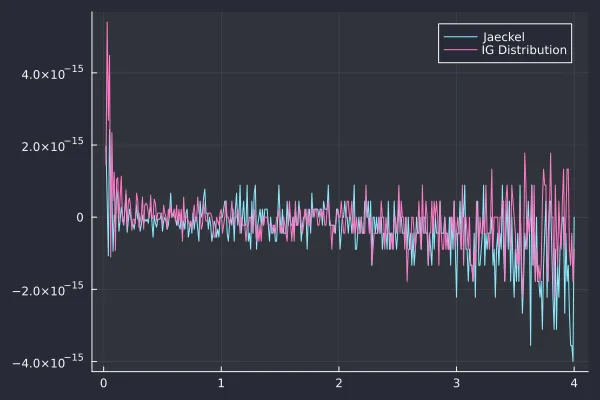

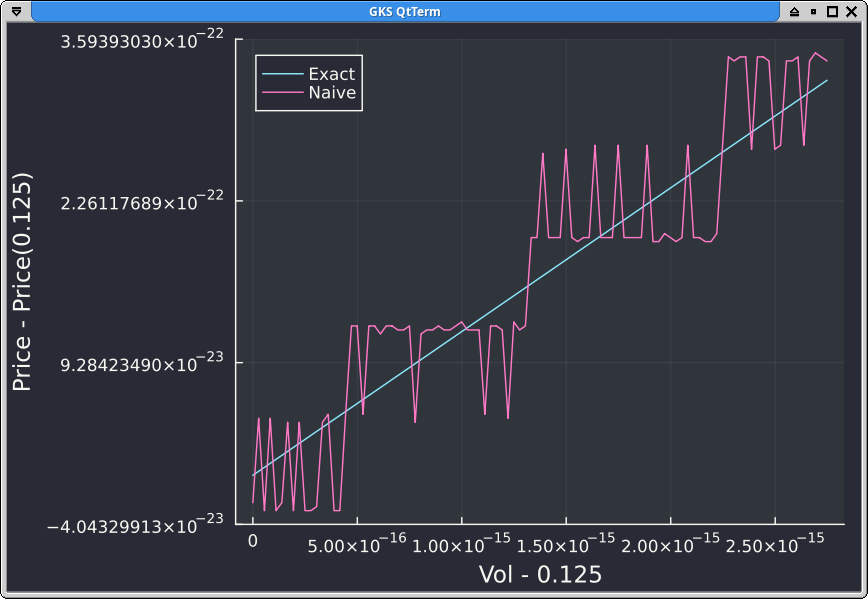

This note compares special-function choices at the level that matters to the implied volatility solvers : the normalized Black beta price, not standalone erfcx(x) . For x = log(F/K) <= 0 and total volatility s = sigma sqrt(T) , the beta-space OTM call price is B(x, s) = 0.5 * (exp(x/2) * erfc(q1) - exp(-x/2) * erfc(q2)) q1 = -(x/s + s/2) / sqrt(2) q2 = -(x/s - s/2) / sqrt(2) The corresponding for…

Chase the Devil

algorithmic-tradingquant-financerisk-management

quant-financerisk-managementvolatility-modeling

algorithmic-tradingquant-financerisk-management

algorithmscomputer-science

aideep-learning

mathematicsstochastic-calculus

quant-financerisk-management

quant-financestochastic-calculus

algorithmic-tradingquant-financestochastic-calculus

quant-financerisk-management

option-pricingquant-financerisk-management

mathematicsoptimization

derivatives-pricingquant-financestochastic-calculus

quant-financerisk-management

derivatives-pricingquant-financestochastic-calculus

algorithmic-tradingquant-financestochastic-calculus

financial-econometricsquant-finance

Sign up to keep scrolling

Create your feed subscriptions, save articles, keep scrolling.

Already have an account?