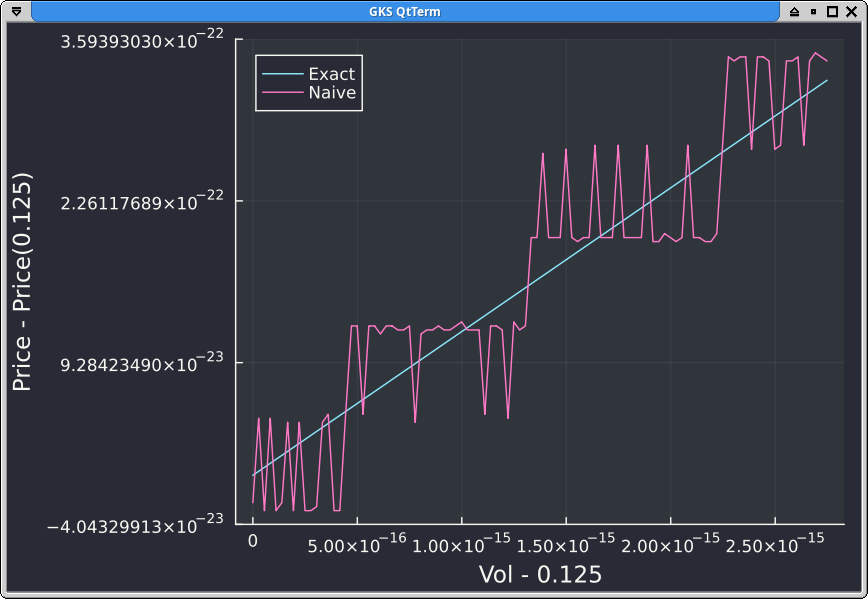

It is well known that vanilla option prices must increase when we increase the implied volatility. Recently, a post on the Wilmott forums wondered about the true accuracy of Peter Jaeckel implied volatility solver, whether it was truely IEEE 754 compliant. In fact, the author noticed some inaccuracy in the option price itself. Unfortunately I can not reply to the forum, its login process does not seem to be working anymore, and so I am left to blog about it.