In the paper "The GARCH OPTION PRICING MODEL", Duan(1995) developed a pricing model for options on an asset whose returns follow GARCH process. Let $X_t$ be the asset price at time t, its process is modeled under physical measure P as GARCH(1,1)-M: $$

ln(\frac{X_t}{X_{t-1}})=r+\lambda \sqrt{h_t} -0.5h_t+\epsilon_t \quad (2.1)\\

\epsilon_t|\phi_{t-1} \sim N(0,h_t) \\

h_t = \alpha_0 +\alpha_1 \epsi…

I am trying to price the following call option using the UVM method in R. The code I wrote below keeps producing the same price for the min and max volatilities, which is wrong, however, I can't seem to fix this error. # Market Data

strike_call <- c(150,152.5,155,157.5,160,165,170,172.5,175,177.5,180,182.5,185,187.5,190,192.5,195,197.5,200,202.5,205,207.5,210,212.5,215,217.5,220,222.5,225,227.5,2…

I want to calculate implied volatility of american option of a short term interest rate future. Let's take for example a put option for a SOFR future with $K=95, price=0.105, T=0.750685, underlying=95.505$ I currently use as a first approximation the implied vol by using finding implied vol using the Bachelier model (used to price European options from my understanding). The undiscounted price fo…

I got an American put option, where the payoff is $V_\tau = \max(K - X_{\tau}, 0)$ and $X_{\tau}$ is the price of an underlying at the stopping time $\tau < T$ . The underlying follows a standard GBM with $r = q = 0$ ; $X_0$ is given. I need to calculate the expectation $E[V]$ under the assumption that $\tau$ has exponential distribution with intensity $\lambda = 0.025$ . I tried transforming thi…

I'm trying to replicate how Bloomberg's OVML prices options. My guess is whenever I'm solving for IV, I'm passing a premium that's too cheap, that's why the IV I solve overcompensates. This is probably because I'm discounting the premium improperly. Same goes with the Premium being cheaper than the actual deal. Here's the sample deal I'm trying to validate my pricer with using OVML. # Sample Deal…

It is well known that vanilla option prices must increase when we increase the implied volatility. Recently, a post on the Wilmott forums wondered about the true accuracy of Peter Jaeckel implied volatility solver, whether it was truely IEEE 754 compliant. In fact, the author noticed some inaccuracy in the option price itself. Unfortunately I can not reply to the forum, its login process does not…

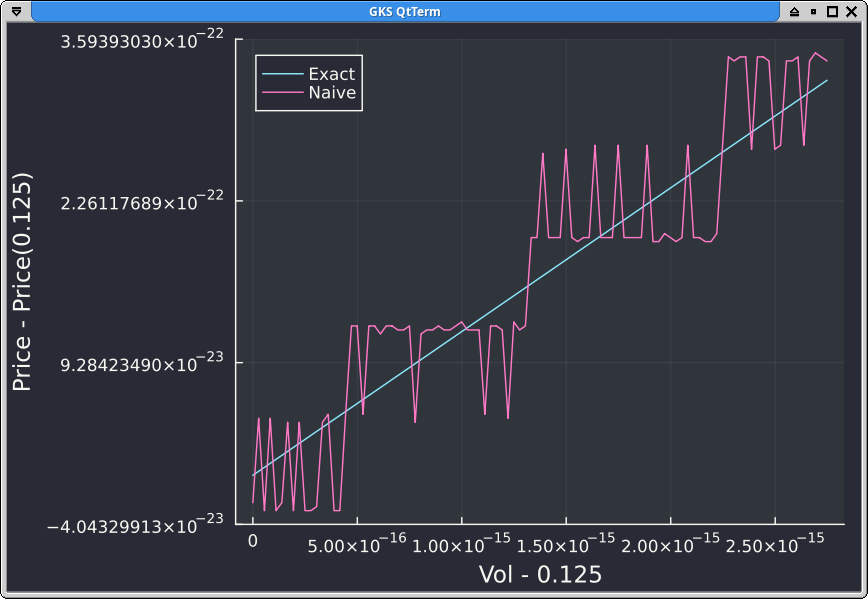

I have implemented a finite difference scheme for pricing options using a Black-Scholes-like model. I tested my implementation on a call option, and found that it gave extremely inaccurate results. I investigated intermediate values in my computations, and I suspect that my inaccurate results are caused by the discontinuity in the payoff function. The payoff function: $$\text{Payoff}(S) = \max(S-…

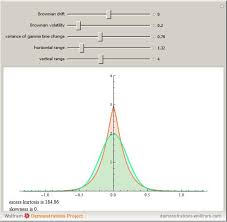

The research in this post and the related paper on Range Based EGARCH Option pricing Models is focused on the innovative range-based volatility models introduced in Alizadeh, Brandt, and Diebold (2002) (hereafter ABD). We develop new option pricing models using multi-factor diffusion approximations couched within this theoretical framework and examine their properties in comparison with … Contin…

You've just tried to access content that is only available to WILMOTT INNER CIRCLE members! Membership of WIC is a simple, free, upgrade to ordinary membership of wilmott.com. All we need is a bit more personal [...]

There’s been a lot of criticism of the Black-Scholes model of late, on our Forum, in our blogs, in the magazine (see Haug & Taleb, Wilmott magazine, January 2008) and in other media. Most is [...]