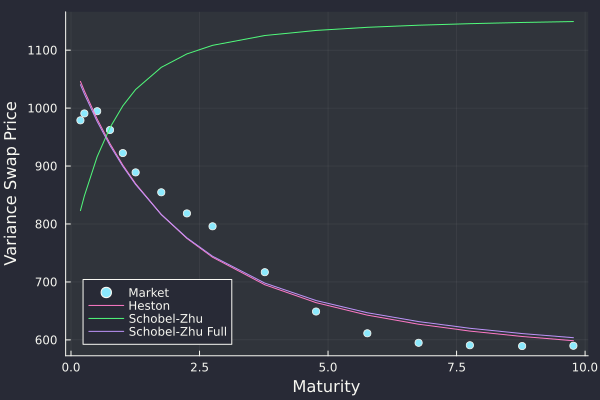

I never paid too much attention to it, but the term-structure of variance swaps is not always realistic under the Schobel-Zhu stochastic volatility model. This is not fundamentally the case with the Heston model, the Heston model is merely extremely limited to produce either a flat shape or a downward sloping exponential shape. Under the Schobel-Zhu model, the price of a newly issued variance swap reads $$ V(T) = \left[\left(v_0-\theta\right)^2-\frac{\eta^2}{2\kappa}\right]\frac{1-e^{-2\kappa T}