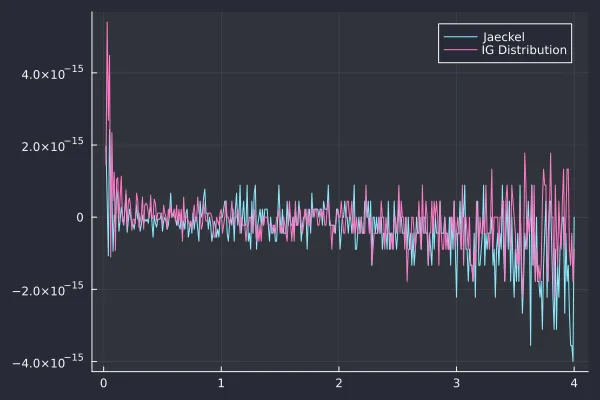

Several years ago, I had explored accuracy and performance of different ways to imply the Black-Scholes volatility. Jherek Healy proposed some improvements over my naive algorithm on his blog . Recently, a Linkedin post mentioned a new paper from Wolfgang Schadner which presents an almost explicit formula for the implied volatility. Almost because it actually relies on some implementation of the quantile function for the inverse Gaussian distribution: it requires a specialized numerical algorith