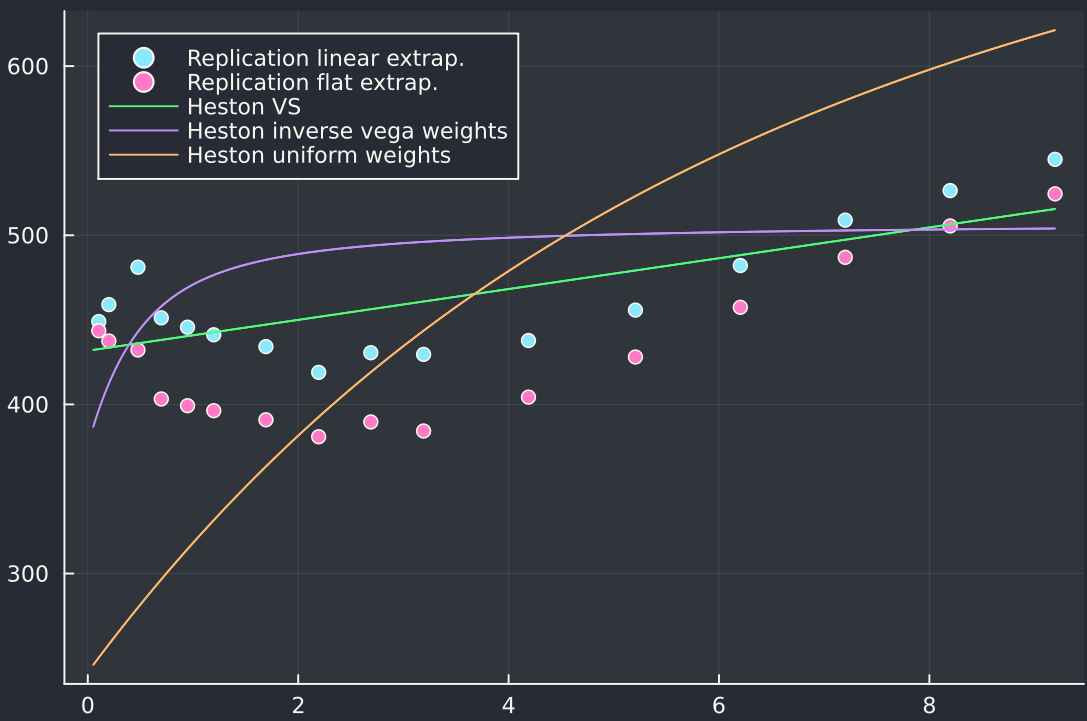

An interesting idea to calibrate the Heston model in a more stable manner and reduce the calibration time is to make use of variance swap prices. Indeed, there is a simple formula for the theoretical price of a variance swap in the Heston model. It is not perfect since it approximates the variance swap price by the expectation of the integrated variance process over time. In particular it does not take into account eventual jumps (obviously), finiteness of replication, and discreteness of observ