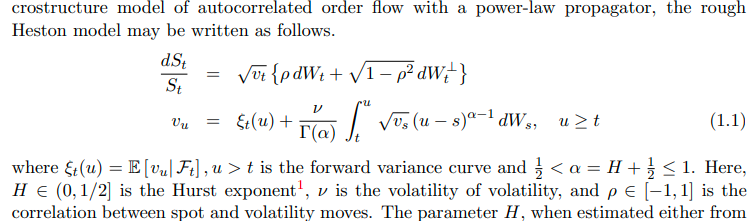

The modern rough volatility models adopt a forward variance curve terminology (see for example this paper on a rational approximation for the rough Heston, or this presentation on affine forward variance models or this paper on affine forward variance models). In this form, the rough Heston model reads: According to the litterature, the initial forward variance curve is typically built from the implied volatilities through the variance swap replication: for each maturity, the price of a newly is