credit-riskquant-financerisk-management

credit-risk

Global Trading

Risk Management Association of India

credit-riskquant-finance

Frontiers in Artificial Intelligence | New and Recent Articles

Naresh Adhikari

20d ago

aialgorithmic-tradingcredit-riskmachine-learningquant-finance

Towards Data Science

credit-riskquant-financerisk-management

Credit Benchmark

credit-riskquant-financerisk-management

SOPHIE's Daddy Quant Blog

credit-riskfinancial-econometricsquant-financerisk-management

International Swaps and Derivatives Association

Christopher Faimali

5/5/2026

credit-riskquant-finance

Recent Questions - Quantitative Finance Stack Exchange

user3762120

5/3/2026

credit-riskquant-finance

Recent Questions - Quantitative Finance Stack Exchange

credit-riskquant-financerisk-management

Credit Benchmark

credit-riskquant-finance

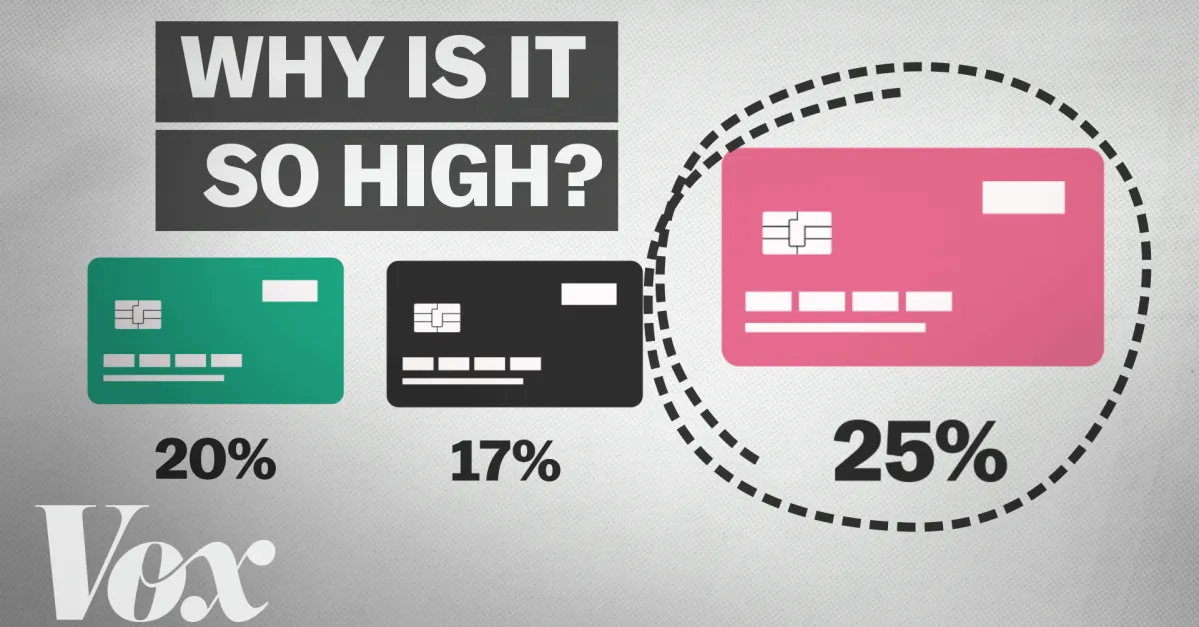

Vox

credit-riskeconomics

DEV Community

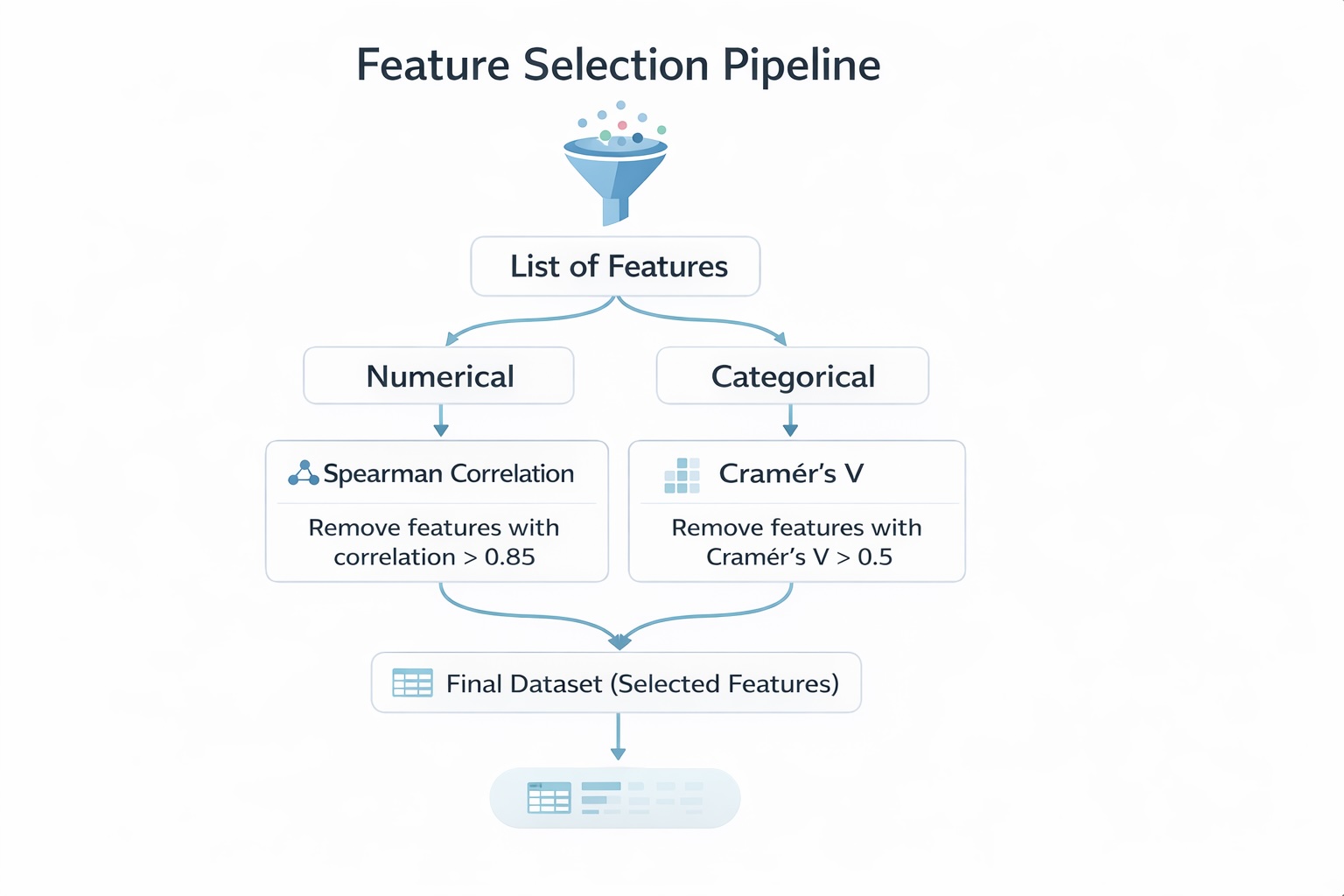

credit-riskquant-finance

Towards Data Science

credit-riskquant-finance

Credit Benchmark

credit-riskquant-finance

AccountingAdaptabilityAnalyticsAsset (computer security)Business, Management and Accounting

Credit Benchmark

credit-riskquant-financerisk-management

Z

Zenodo (CERN European Organization for Nuclear Research)

Asset (computer security)Asset qualityBanking stability, regulation, efficiencyCredit riskEconomics, Econometrics and Finance

A

arXiv (Cornell University)

Climate changeClimate riskCredit riskEconomics, Econometrics and FinanceEnvironmental hazard

Z

Zenodo (CERN European Organization for Nuclear Research)

Paper

YASIN KALAFAOGLU

3/23/2026

AccountingBusiness, Management and AccountingCredit riskDecision analysisDecision rule

Markets Media

credit-riskquant-finance

Sign up to keep scrolling

Create your feed subscriptions, save articles, keep scrolling.

Already have an account?