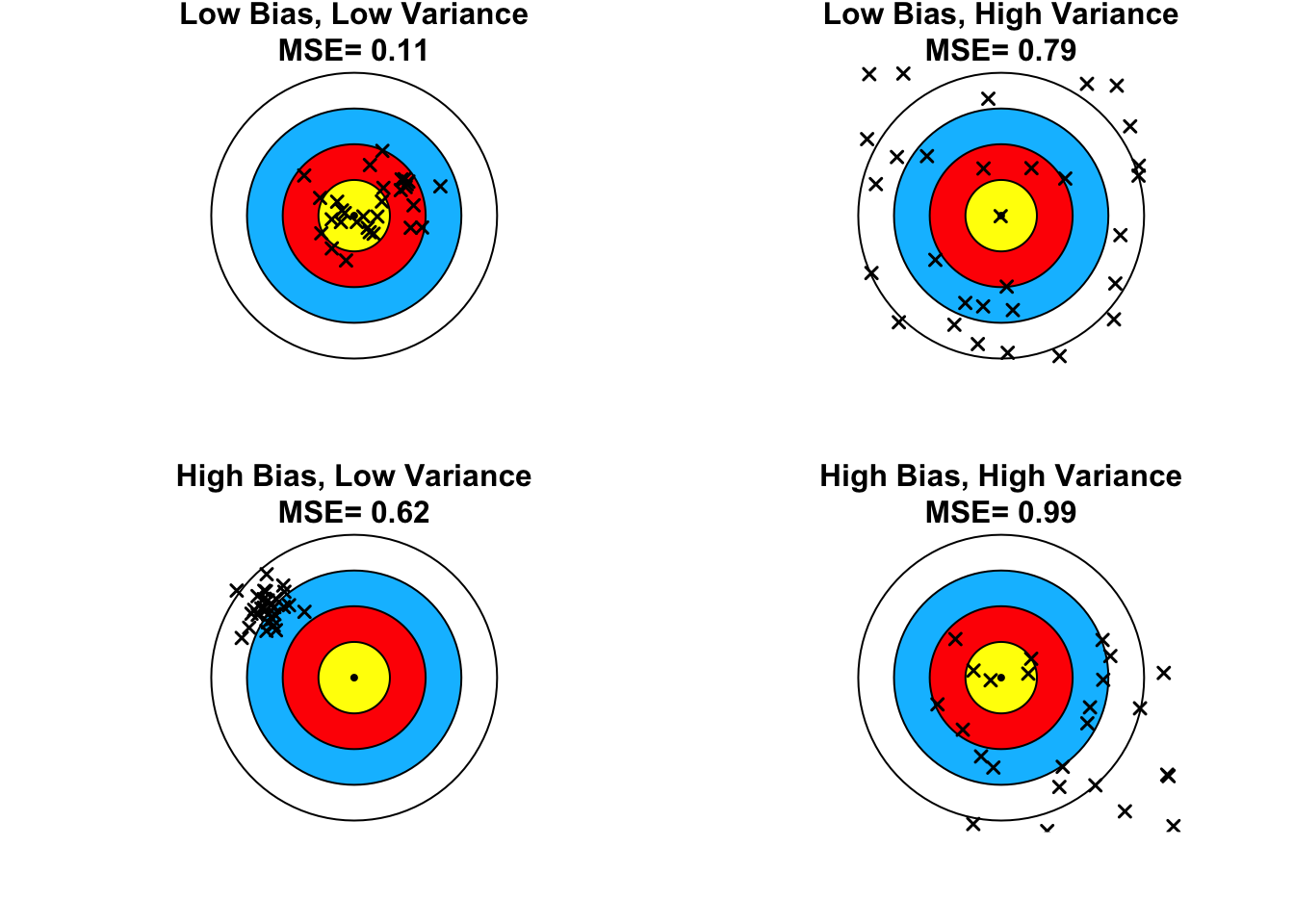

If you study enough econometrics or statistics, you’ll eventually hear someone mention “Stein’s Paradox” or the “James-Stein Estimator” . You’ve probably learned in your introductory econometrics course that ordinary least squares (OLS) is the best linear unbiased estimator (BLUE) in a linear regression model under the Gauss-Markov assumptions. The stipulations “linear” and “unbiased” are crucial here. If we remove them, it’s possible to do better–maybe even much better –than OLS. 1 Stein’s para