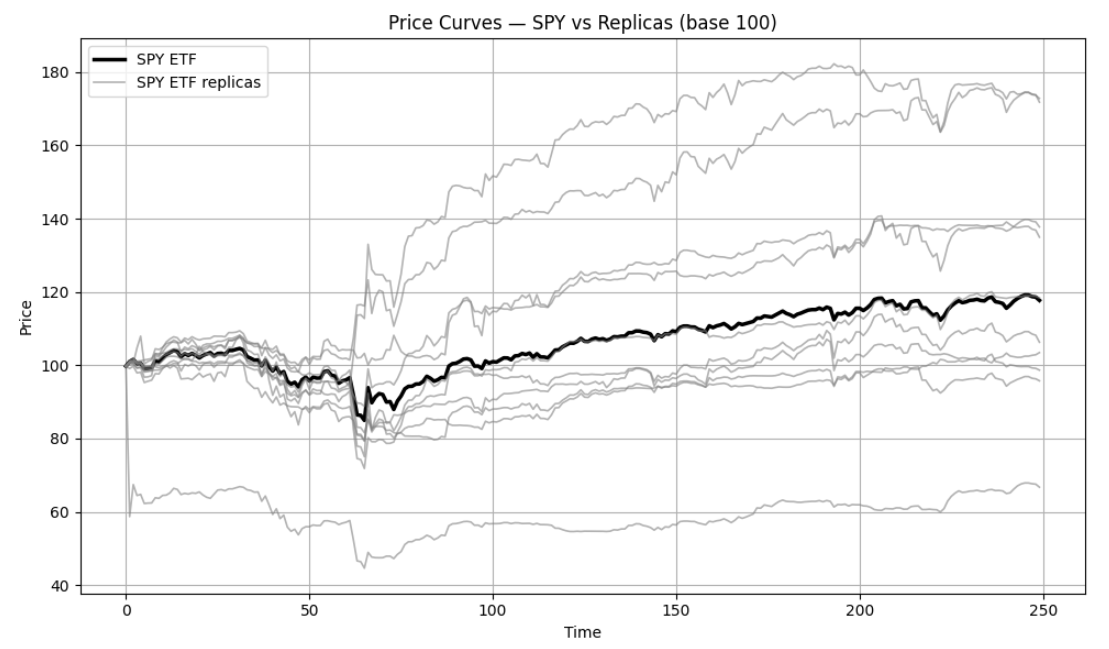

In a previous article, I described several classical bootstrap techniques — i.i.d. bootstrap, circular block bootstrap, and stationary block bootstrap — and showed how the stationary block bootstrap could be used to simulate future price paths for financial assets by following the methodology of Anarkulova et al.1. In this blog post, I will detail another bootstrap technique called the autoregressive online bootstrap2 and introduced in Palm and Nagler2, that is best described as a multiplier boo

More Bootstrap Simulations with Portfolio Optimizer: the Autoregressive Online Bootstrap

Roman R.