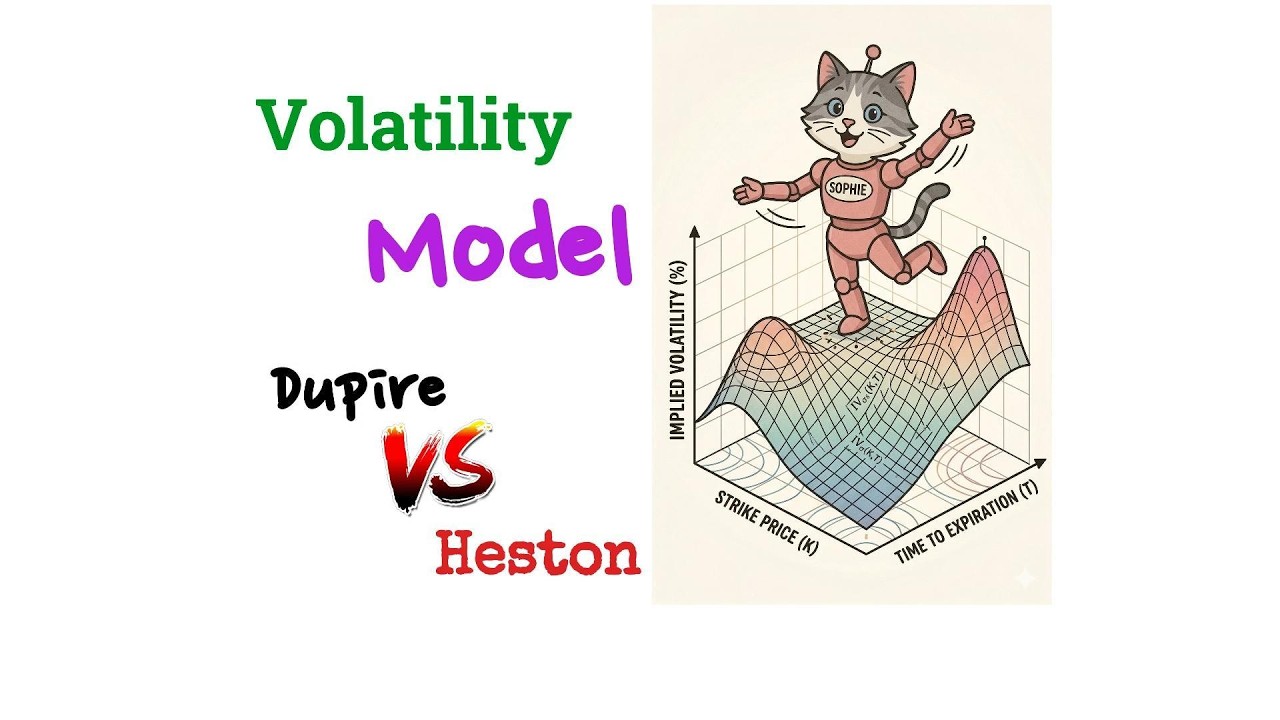

This video traces the evolution of volatility modeling from Black-Scholes to modern surface calibration, covering SVI parametric models, Dupire local volatility, and the Heston stochastic volatility framework with practical derivative pricing applications.

🎥 Video Tutorial • 📈 Options Strategy

🎥 Watch Video: https://youtu.be/EjaO4UaVLJA

Topics: quantitative finance, investment analysis, financial education, options trading, derivatives