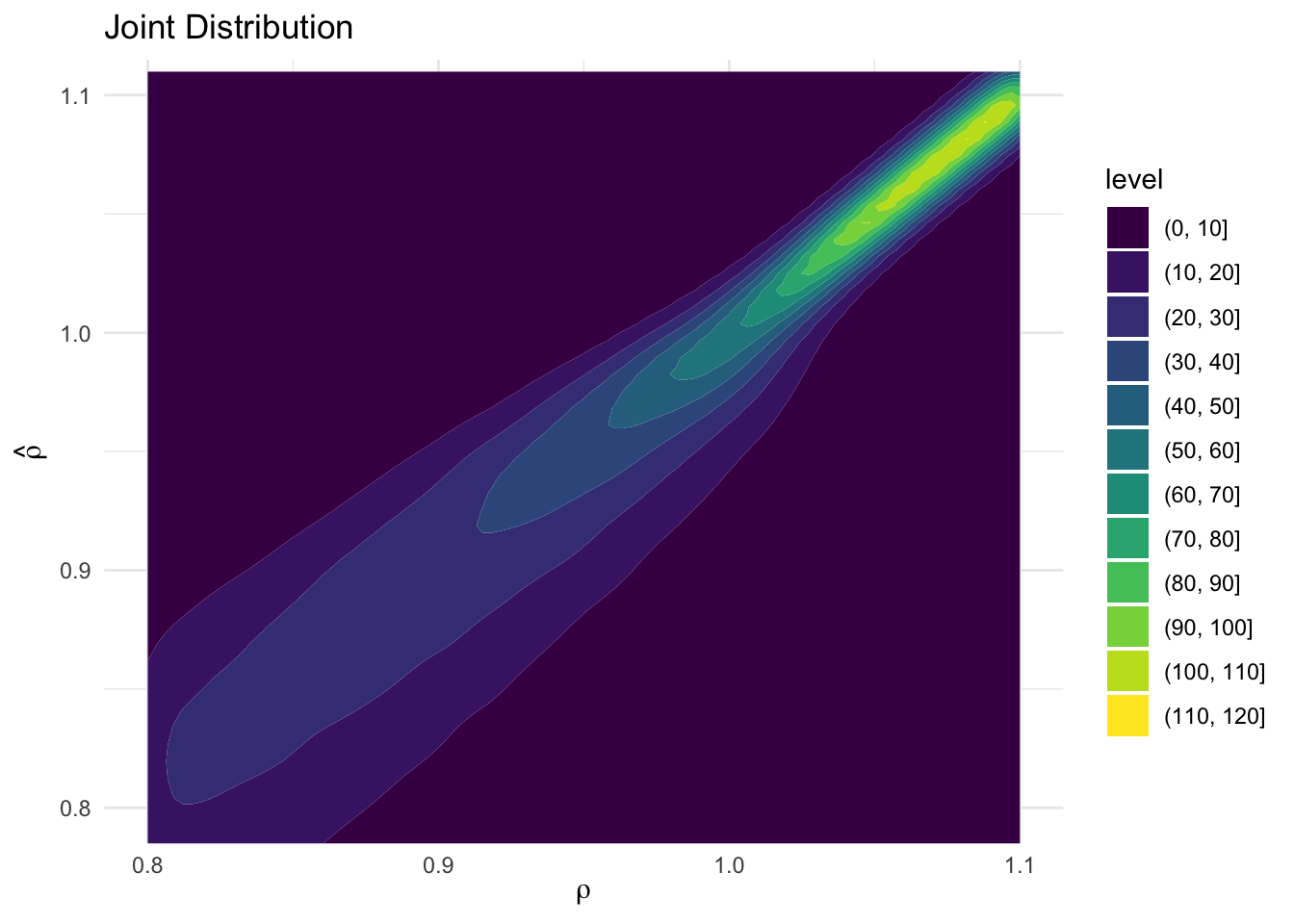

As a teaser for our upcoming (2024-07-23) virtual reading group session on Bayesian macro / time series econometrics, this post replicates a classic paper by Sims & Uhlig (1991) contrasting Bayesian and Frequentist inferences for a unit root. In the post I’ll focus on explaining and implementing the authors’ simulation design. In the reading group session (and possibly a future post) we’ll talk more about the paper’s implications for the Bayesian-Frequentist debate and relate it to more recent w